LIFOis most suitable when you want to match current costs with current revenues. LIFO assumes you will sell the most recently acquired inventory first, making it best for businesses that want to reflect the current cost of goods sold. The difficulties are compounded when trying to maintain uniform pricing across channels while accounting for these varying costs. For instance, online sales might incur additional shipping and handling fees, which do not apply in physical stores. Similarly, promotional activities exclusive to one channel can disrupt standard cost calculations, affecting overall profitability analysis. If the prices of the products your business buys hardly change, then your accountant can use an even easier method called Weighted Average Costing.

What are the main inventory valuation methods?

However, if your stock volumes are smaller, the average cost method may be sufficient and easier to manage. On the other hand, the weighted average cost method takes into account the quantity of each item, thereby providing a more accurate reflection of COGS and ending inventory. The average cost method is quite self-explanatory, meaning that explanation of certain schedule c expenses it calculates the average cost of all items in inventory, regardless of the quantity. This method is simpler and faster than the weighted average cost method but doesn’t always provide as much accuracy in terms of COGS and ending inventory. However, it’s difficult to achieve unless items are distinct and their costs are easily traceable.

Capital costs

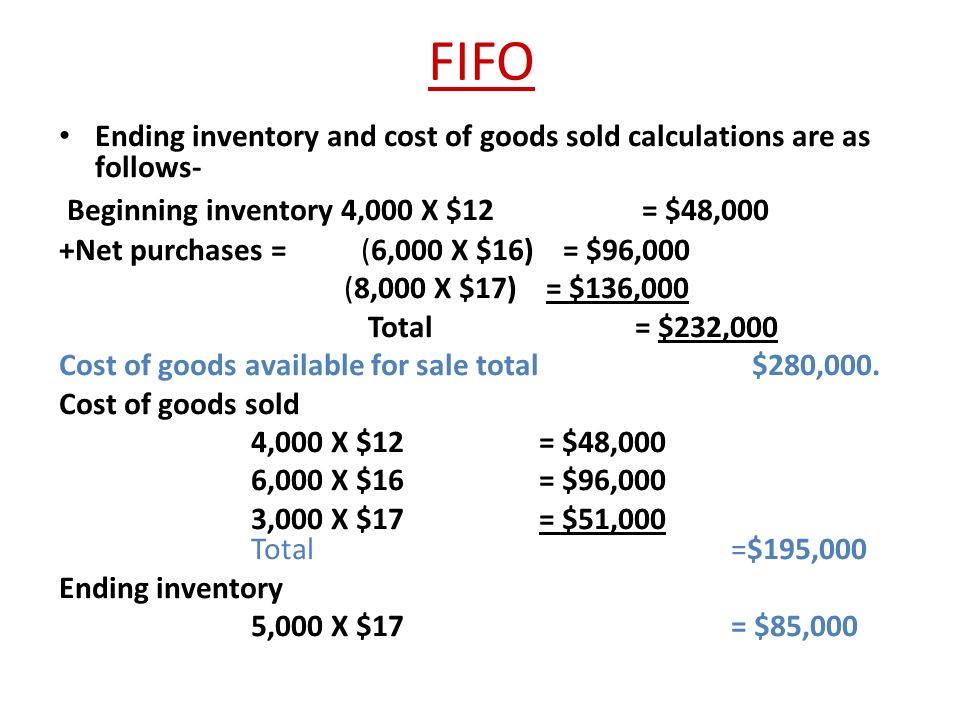

Since FIFO assumes that the first items purchased are sold first, the latest acquisitions would be the items that remain in inventory at the end of the period and would constitute ending inventory. The best inventory costing method depends on your business but the most popular is FIFO (first-in, first-out), as it usually provides the most accurate view of COGS (cost of goods sold) and gross profit. For each of the methods, we’re going to use Ariana’s Accessories as an example. Let’s look in more detail at a three-month account period from July to September using each of the inventory costing methods.

WAC: Average cost per unit

In the next purchase, the store buys 50 more smartphones, once again at $220 each. “Let’s say someone sells unique paintings that they buy from local artists and then sells,” says Abir.

Why is inventory valuation important?

Read on to learn about each inventory valuation method and how you can choose one that’s right for your business. Like IAS 2, transport costs necessary to bring purchased inventory to its present location or condition form part of the cost of inventory. Unlike IAS 2, US GAAP does not contain specific guidance on storage and holding costs, which may give rise to differences from IFRS Standards in practice. In general, US GAAP does not permit recognizing provisions for onerous contracts unless required by the specific recognition and measurement requirements of the relevant standard. However, if a company commits to purchase inventory in the ordinary course of business at a specified price and in a specified time period, any loss is recognized, just like IFRS Standards.

- If you spend $12,000 on two orders that resulted in 15,000 juices, the average price per juice is $0.80.

- Generally accepted accounting principles (GAAP) and the International Financial Reporting Standards (IFRS) apply to both.

- The first-in, first-out method (FIFO) records costs relating to a sale as if the earliest purchased item would be sold first.

- As you can see, the inventory method a company uses affects its cost of goods sold, which impacts profitability.

Usually, you calculate inventory valuation at the end of every financial year to calculate the cost of goods sold and the cost of any unsold inventory. Understanding the four main types of inventory valuation will help you decide which is best for your growing mid-size business. Each inventory valuation method has a unique set of pros and cons making it better suited to certain industries and business structures. Transportation costs are commonly assigned to either the buyer or the seller based on the free on board (FOB) terms, as the terms relate to the seller. Transportation costs are part of the responsibilities of the owner of the product, so determining the owner at the shipping point identifies who should pay for the shipping costs. The seller’s responsibility and ownership of the goods ends at the point that is listed after the FOB designation.

Remember, specific identification is not a cost-flow assumption, but it is still a GAAP- and IFRS-accepted technique for inventory costing. The two main metrics inventory costing determines are cost of goods sold (COGS) and ending inventory balance (remaining inventory cost at the end of an accounting period). The pros and cons of the specific identification method depend on the size of your retail business, according to the Corporate Finance Institute (CFI). For the specific identification method to suit your retail business, you need to be able to confidently and accurately identify the location, cost, and sale amount of every stock-keeping unit (SKU) in your inventory. That’s where inventory costing (also known as inventory valuation) comes in. Inventory costing gives your business an accurate picture of what is likely your largest asset, which is crucial for informed financial decisions.

The remaining assets in the inventory are matched to assets that are most recently produced or purchased. The costs necessary to bring the inventory to its present location – e.g. transport costs incurred between manufacturing sites are capitalized. The accounting for the costs of transporting and distributing goods to customers depends on whether these activities represent a separate performance obligation from the sale of the goods. IAS 2 requires the same cost formula to be used for all inventories with a similar nature and use to the company, even if they are held by different legal entities in a group or in different countries. In practice, for an acquired business this often requires rapid realignment to its new parent’s group methodologies and systems.